Publications

Are Chinese investments in solar energy in the Middle East a response to market demand or part of a calculated geopolitical strategy, and what is their significance for Israel?

INSS Insight No. 2150, June 7, 2026

Follow us on GoogleSince the outbreak of the war with Iran in February 2026, and the blockade of the Strait of Hormuz which led to a decline in global oil supply, the demand for solar energy has grown at an unprecedented rate. In March, at the height of the war, China exported solar panels with a total rated capacity of 68 gigawatts (GW) — twice China’s solar exports in February, and 49% higher than the previous record set in August 2025. Oil-dependent countries around the world are accelerating their renewable energy programs, and in the Middle East this trend aligns with long-term plans for economic and energy diversification. China, which holds more than 80% of the global solar supply chain, is the main beneficiary of this trend. Yet behind this picture lies a question that has thus far received insufficient attention: Are China’s investments in solar energy in the Middle East merely a response to market demand, or are they part of a broader geopolitical strategy, and what are the implications for Israel?

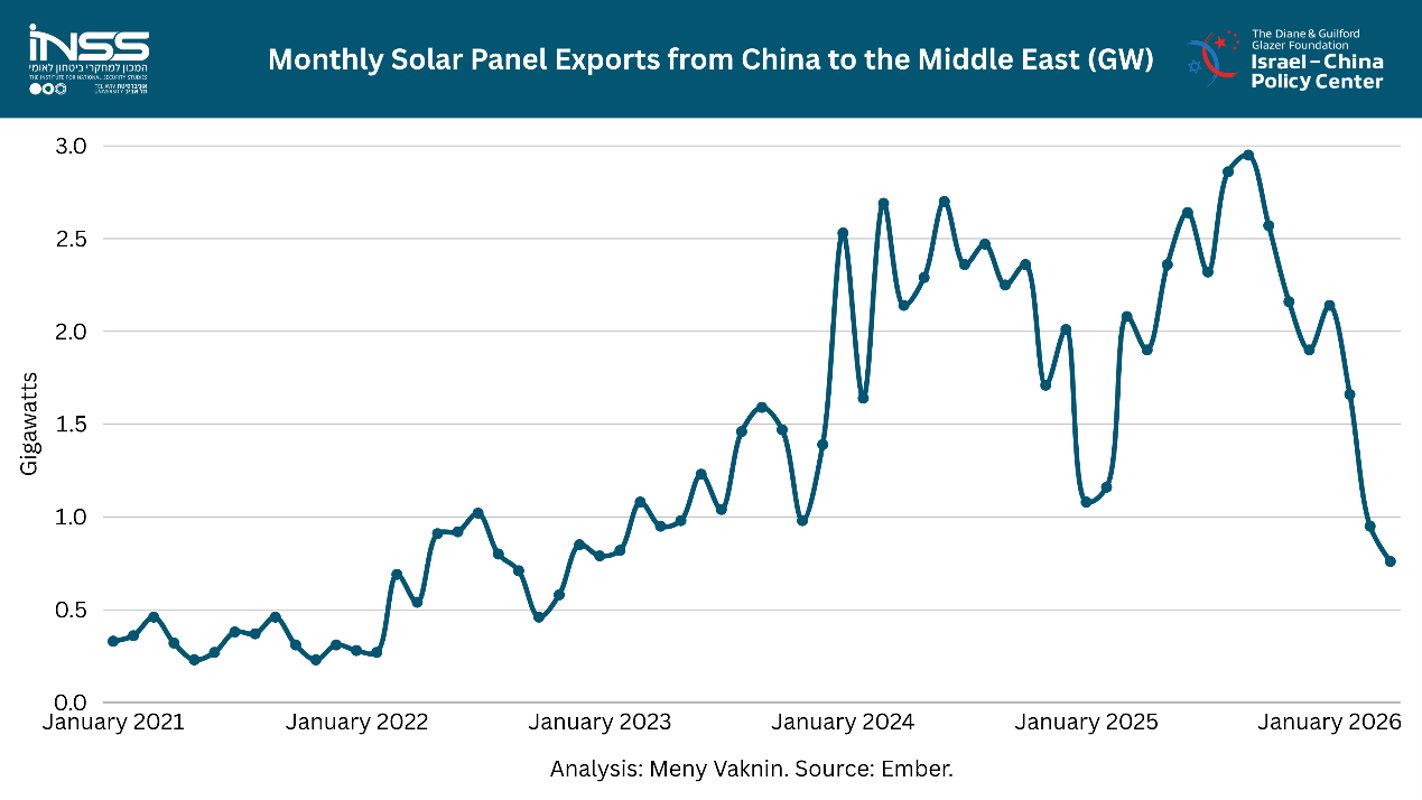

The recent surge in Chinese solar energy exports is not coincidental. It rests on a strategy that China has built patiently since 2016: a systematic penetration of the Middle East solar energy market, while combining economic, geopolitical, and security motives. China does not view solar energy merely as an environmental tool but as a strategic asset, and the war with Iran illustrates the relevance of this approach. As the energy crisis affects many countries, demand for solar power — whose supply chain is overwhelmingly dominated by China — is rising as a partial solution, particularly for electricity generation. In January 2021, monthly Chinese exports of solar panels to the Middle East stood at only 0.33 GW. Five years later, in January 2026, monthly exports to the region increased 6.5 times, reaching 2.14 GW (see Figure 1).

China's Strategic Motives in the Middle East

The Chinese strategy in the solar sector encompasses several complementary dimensions, the first of which is economic. In 2023, Chinese companies produced panels with a total rated capacity of approximately 700 GW, three and a half times the amount of panels installed in China itself. This overproduction, driven by a generous government subsidy policy, led to a sharp decline in prices and heavy losses: China's five largest solar panel manufacturers laid off roughly 30% of their workforce during 2024. At the same time, Middle Eastern markets, characterized by surging demand from states with high fiscal capacity, provide a significant export destination for Chinese industry. The war in Iran intensified this pressure: as noted above, global demand for solar energy jumped sharply in 2026, giving Chinese companies that suffered heavy losses an opportunity to recover. This was the case even though most of the growth occurred mainly outside the Middle East, which was affected by the closure of the Strait of Hormuz.

The second dimension of China's solar strategy concerns circumventing trade barriers. The European Union and the United States have imposed tariffs on Chinese solar panels, alleging unfair trade practices. In response, China moved part of its production lines to third countries — initially to Southeast Asia and, in recent years, to Saudi Arabia, the United Arab Emirates, and Turkey. Because these countries maintain favorable relations with the West, Beijing assesses that products manufactured there will be less vulnerable to tariffs. The establishment of a solar panel manufacturing facility in Turkey by the Chinese company Astronergy, backed by a $500 million investment and expected to be completed by 2028, and Egypt's signing in August 2025 of a $220 million agreement to establish a solar panel manufacturing complex in Suez in partnership with China, are examples of this strategy. In both cases, these are not merely commercial transactions but the establishment of manufacturing infrastructure beyond China's borders, with the additional objective of reducing exposure to future sanctions and tariffs.

Beyond economic considerations, these investments serve the purpose of shaping an international image. China is the world's largest emitter of greenhouse gases and continues to increase its coal consumption year after year. Investments in solar energy allow Beijing to promote a counter-narrative. In 2007, former Chinese President Hu Jintao introduced the concept of an "ecological civilization," which current President Xi Jinping has adopted as a central pillar of Chinese policy. At a time when the United States is reducing its involvement in climate policy and renewable energy incentives, China is working to position itself as the leading power of the "Global South" in the field of clean energy. The "Green Belt and Road Initiative" — the framework through which China promotes its energy projects — lends this activity prestige and a narrative of global partnership. In Middle Eastern countries, some of which maintain a degree of distance from the West, this narrative has gained relatively broad acceptance and has strengthened confidence in Chinese companies as long-term partners.

Beyond image-building, China's strategy also contains a deeper geopolitical dimension: advancing a multipolar international order in which American hegemony is balanced by additional actors. While the United States' military presence in the Persian Gulf provides it with significant influence, China competes in the economic and technological arenas — areas in which its solar advantage constitutes a genuine strategic asset. The war in Iran illustrates the operability of this vision: as the United States leads a military campaign that disrupts the stability of regional energy supplies, China presents itself as a provider of a complementary, long-term energy solution. As a result, many countries, including those that have territorial and security disputes with China, have chosen to deepen their dependence on it due to the absence of a readily available alternative.

Finally, China's policy in the Middle East can also be examined as a mechanism for ensuring energy security. China is a major, and in some cases even the largest, customer of oil from Saudi Arabia, the United Arab Emirates, Iran, and Iraq. Chinese solar investments deepen economic ties with these countries and strengthen the frameworks of bilateral cooperation upon which the flow of oil and gas to China relies. The blockade of the Strait of Hormuz, which exposed the fragility of the global energy supply chain, further sharpens China's interest in diversifying its energy sources and deepening its relations with regional oil exporters. Thus, Chinese solar investment and its fossil-fuel-based energy security complement rather than contradict one another.

However, the war in Iran exposed a limitation in China's strategy. While global demand for solar energy spiked in March 2026, the Middle East did not experience a corresponding increase in the import of Chinese solar panels, due to disruptions in maritime trade routes associated with the blockade of the Strait of Hormuz. This vulnerability stems from the fact that the regional solar supply chain is not yet independent: some of the local manufacturing facilities that China is establishing in the region are not yet fully operational, and those that are already operating remain dependent on core components manufactured in China, including polysilicon, solar cells, and other intermediate components. As long as regional production relies on maritime transport from China, the blockade of the Strait of Hormuz directly undermines China's ability to supply the Middle Eastern market. Consequently, exactly when demand for its products is increasing, China finds itself struggling to supply them to a market that is central to its regional strategy.

Gradual Presence: The Pattern of Chinese Entrenchment in the Regional Solar Market

Across the Middle East, Chinese activity manifests through three approaches: first, the export of solar panels and components at a competitive price; second, the construction of power plants through joint ventures with local government entities, thereby creating a long-term operational presence; and third, the establishment of local manufacturing facilities for solar panels and inverters, which deepens technological dependence while also enabling the circumvention of Western tariffs. These approaches are fully implemented in certain countries, while in others they are adopted only partially, depending on local conditions. The significance is not merely a dependence on importing panels, but the emergence of a multi-layered form of dependence: commercial dependence on components, operational dependence on control and maintenance systems, and strategic dependence on relationships with Chinese companies and government entities.

Figure 1:

Saudi Arabia and the United Arab Emirates are examples of the full integration of all three approaches. In 2025, Saudi Arabia reached approximately 12.7 GW of installed solar capacity, an increase from just 700 megawatts in 2022. This growth also reflects the volume of imports: in 2024, Saudi Arabia alone imported 16.55 GW of Chinese solar panels — more than half of all Middle Eastern imports from China that year. This trend is not unique to Saudi Arabia: as Figure 1 illustrates, total Chinese solar exports to the Middle East have grown at an accelerated and steady rate since 2021, reflecting a gradual deepening of the Chinese presence across the region.

Major solar projects in Saudi Arabia are developed through joint ventures between Chinese companies and the Saudi Public Investment Fund. The most prominent among them is the power plant near Jeddah which, upon completion, will have an installed capacity of 2.6 GW. This facility is expected to become one of the largest solar power plants in the world, alongside additional stations currently in various stages of development across the Kingdom. In the United Arab Emirates, the power plant in Abu Dhabi stands out as the largest single-site solar facility in the world at 2 GW, built and operated by a Chinese state-owned company. This is complemented by Dubai's massive solar park, which integrates multiple solar technologies and has an installed capacity of approximately 2.86 GW.

Egypt and Turkey represent a different model: Chinese activity in these countries focuses on the third approach — the establishment of manufacturing facilities in cooperation with China. In August 2025, Egypt signed a $220 million agreement to establish a solar panel manufacturing complex in Suez, an economic zone that is increasingly emerging as a regional solar manufacturing hub, in collaboration with Chinese, Emirati, and Bahraini partners. Turkey also hosts several Chinese-owned solar panel manufacturing facilities. Jordan, by contrast, represents an exceptional case — most of the country's solar projects are built by Western companies, and in April 2025, Jordan launched an anti-dumping investigation into imported Chinese panels, illustrating that China's strategy has not achieved uniform success across every market. The broader regional picture clearly points toward a deepening partnership with China in the solar sector, a trend that the war in Iran is expected to accelerate even further.

Israel in the Shadow of China's Strategy: Opportunities, Constraints, and Risks

In the context of solar energy, Israel represents a unique case compared to other countries in the region: a Western country with advanced technological capabilities, that was the first in the Middle East to produce solar electricity on a commercial scale, yet one that currently lags behind the targets it set for itself. Approximately 11% of Israel's electricity is produced from solar energy, while renewable energy sources as a whole account for roughly 15% of the country's electricity mix — falling short of the government's 2025 target of 20%.

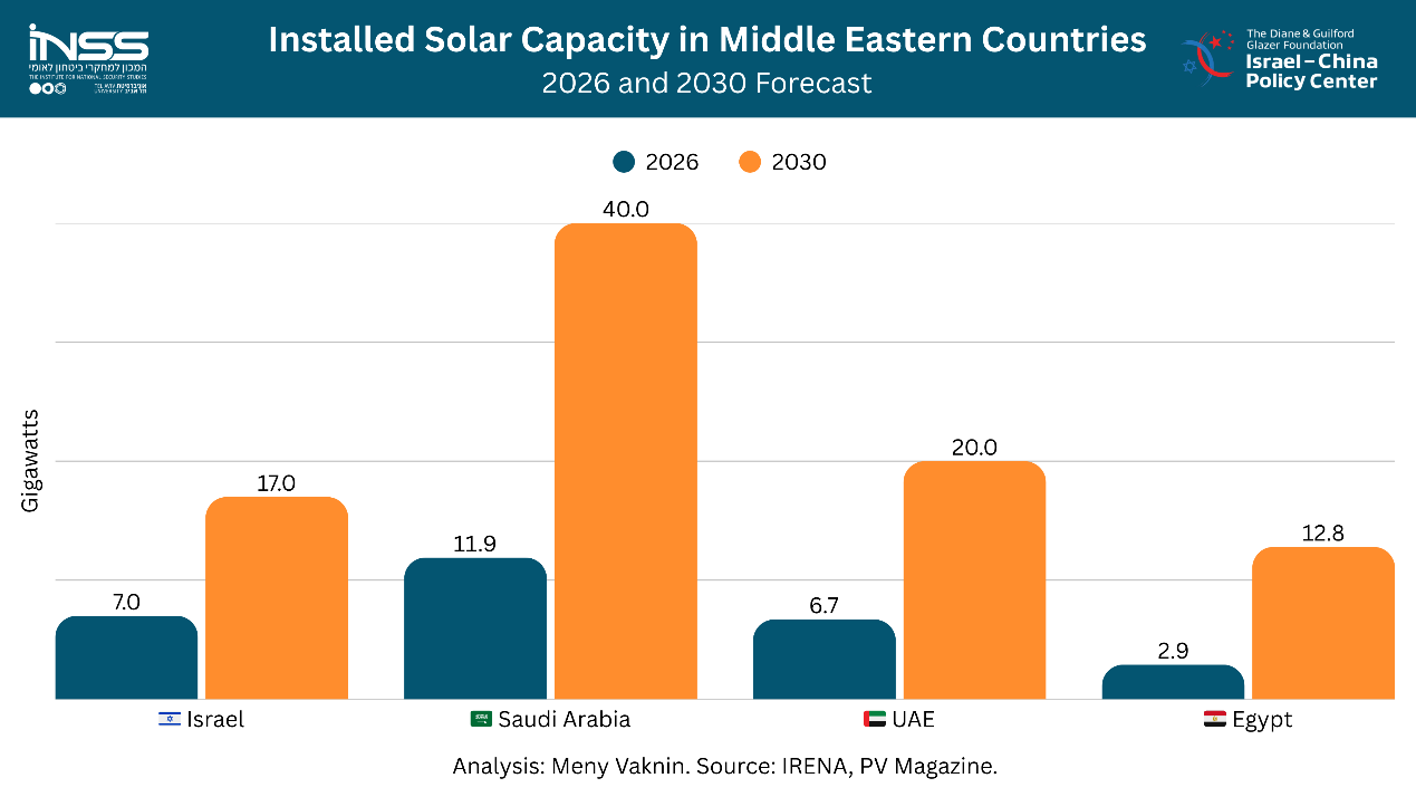

Against this backdrop, a regional comparison reveals a complex picture. In terms of the share of solar energy in the electricity generation mix, Israel still maintains a relatively favorable position compared to some Middle Eastern countries: solar energy accounts for only 2% of the electricity mix in Saudi Arabia and about 9% in the United Arab Emirates. However, this relative advantage is expected to shrink, and may even be reversed, in the coming years. Both Gulf states are currently setting up projects on a scale of tens of gigawatts, primarily in cooperation with Chinese companies, and their installed solar capacity is expected to exceed Israeli capacity by a considerable margin by 2030. As Figure 2 demonstrates below, the projected gap by 2030 is dramatic: while Israel is expected to reach about 17 GW of planned solar capacity, Saudi Arabia and the United Arab Emirates are projected to reach 40 GW and 20 GW, respectively. This gap stems from a combination of vast land area, government capital, and extensive cooperation with Chinese firms.

Israel, by contrast, faces geographic constraints, with a population density of 440 people per square kilometer compared to just 16 in Saudi Arabia. It also faces political constraints. Jerusalem exercises security caution regarding cooperation with Chinese companies, partly due to American pressure to limit economic ties with Beijing in sensitive sectors. These constraints have effectively limited China's solar presence in Israel to the supply of panels and inverters, without large-scale construction, operation, or local manufacturing projects. The significance is twofold: Israel is not only struggling to meet its renewable energy targets, but it may also find itself losing its regional advantage in the solar sector in the coming years, while its neighbors deepen their economic and technological ties with China through the development of new energy infrastructure.

Figure 2:

At the same time, even this limited level of involvement creates security vulnerabilities. One risk is technological and systemic in nature: most of the inverters installed in Israel are manufactured by various Chinese companies, and in 2019, Huawei alone signed a deal to supply inverters with a capacity of 30 megawatts for solar projects in Israel. An inverter is a computerized component connected to the power grid that manages the interface between solar panels and the national grid, and often includes capabilities for monitoring, software updates, and remote control. As such, it may serve as a potential vulnerability in a cyberattack or enable the exploitation of operational access. To date, there is no documented research evidence of Chinese-made inverters being exploited in Israel. Nevertheless, their widespread presence near sensitive facilities creates a structural vulnerability that warrants regulatory attention.

The fact that Western countries have already begun treating inverters manufactured by suppliers defined as "high-risk" as a sensitive component in energy infrastructure reinforces this need. In Europe, governments have begun restricting support for renewable energy projects that rely on Chinese-manufactured inverters, while in the United States and the United Kingdom, discussions are underway regarding similar restrictions on inverters connected to national power grids. Israel, by contrast, has yet to formulate a dedicated policy on the issue.

A second risk concerns the potential dual-use nature of solar technology. Prior to October 7, 2023, approximately 25% of the electricity in the Gaza Strip was generated by solar systems, largely as a result of frequent disruptions to the Israeli power grid. Some of the panels were installed by private entities, some were funded by the Hamas government, and others were provided through Chinese donations, such as the solar panel system funded by the Chinese government for the Al-Durrah Children's Hospital in 2021. Reports emerging from the war since October 2023 indicate that Hamas has used Chinese-made solar panels to support military infrastructure. This case illustrates that solar energy, often perceived as civilian infrastructure, can become a dual-use technology in the hands of an armed group, and that the nature of its use is dictated by the entity that possesses it. These insights demonstrate that dual-use concerns are not confined to advanced defense technologies alone.

Recommendations for Israel

The two risks outlined above — Chinese-manufactured inverters and dual-use capabilities — require distinct policy responses. The cybersecurity risk relates primarily to components connected to the power grid, including inverters, monitoring systems, and control elements. Israel should ensure that its existing cybersecurity frameworks, particularly the National Cyber Directorate and the relevant regulators within the energy sector, provide a tailored response to the risks arising from the deployment of grid-connected solar equipment. This need stands out particularly when such equipment is installed near sensitive infrastructure. An appropriate response does not necessarily require the establishment of a new solar-specific apparatus or a blanket ban on Chinese equipment. Rather, it would be sufficient to embed security requirements, vendor screening procedures, and risk management protocols within existing licensing and oversight mechanisms.

The question of dual-use panels requires a broader solution. Unlike cybersecurity concerns, it is not unique to equipment originating from China and therefore calls for wider oversight mechanisms governing the transfer of solar equipment to areas where it could potentially be used by armed actors, most notably the Gaza Strip. With regard to supply chains, Israel should avoid presenting supplier diversification as a simple or immediate solution. Given China's dominance of the global solar supply chain, a complete shift to alternative suppliers could prove costly and limited in availability, and even delay renewable energy targets. Therefore, it would be more prudent to pursue a gradual and selective diversification of the most sensitive components — inverters, communication, monitoring, and control systems — while simultaneously mapping existing dependencies and implementing stringent security requirements at sensitive sites. The objective of such a policy should not be to alter China's behavior or impede the transition to renewable energy. Rather, it should be to reduce Israeli vulnerability by enabling the continuous development of the solar energy sector while prudently managing technological dependence, protecting critical infrastructure, and mitigating the potential for hostile use. For Israel, the challenge is not to choose between advancing clean energy and safeguarding national security, but to develop a policy framework that can achieve both.