Publications

Special Publication, May 19, 2026

Follow us on GoogleDespite the prevailing perception that China retreated from the Middle East in 2025 amid the renewed strengthening of the United States in the region and the absence of significant Chinese involvement in the Israel-Iran war, the reality is more complex. A multi-dimensional analysis of trade, investment, technology, as well as security and diplomatic ties, shows that not only has China not retreated from the Middle East, but it has continued to consolidate and deepen its economic foothold there, maintaining a consistent pattern of conduct: avoiding security commitments while expanding economic influence.

The round of confrontation between Israel, the United States, and Iran in early 2026 highlights this trend: China remains a marginal actor in the military arena, yet acts cautiously to leverage the crisis in order to accumulate long-term influence. The central question that remains open is whether and how China will be involved in Iran’s post-war reconstruction—particularly in the rehabilitation of its military capabilities and defense industry. This issue is not merely theoretical. It requires Israel to act in the international sphere alongside regional partners that have also been targeted by Iran, and influence China to refrain from such involvement, particularly with regard to rebuilding Iran’s military capabilities.

Furthermore, Israel must prepare for the intensification of great power competition in the Middle East, potentially in a different and more acute form than that seen over the past decade.

Relations between China and Middle Eastern countries in 2025, on the eve of the 2026 war with Iran, stood first and foremost in the shadow of Donald Trump’s return to the U.S. presidency. At first glance, his term thus far has signaled a significant deepening of United States ties with Middle Eastern countries and, by implication, created the impression of weakening Chinese ties in the region. President Trump’s visit to the Gulf in May 2025 and the massive agreements announced therein—alongside state visits to the U.S. by senior officials from Arab and Muslim nations, including Turkey—positioned the United States as the preeminent partner for these states. Furthermore, certain agreements concerning advanced technology (such as Artificial Intelligence) were reported to explicitly exclude China from cooperation with Arab nations in these fields, with arms supply agreements described in a similar vein.

The Israel-Iran war of June 2025 further cultivated the image of a campaign that weakened China's regional relevance. The absence of significant direct aid to Iran during the conflict, coupled with the modest assistance provided by China in its aftermath (relative to Iran’s expectations), was portrayed as a near-total Chinese retreat from its support for Iran. If Iran was described as a "paper tiger," China was depicted as merely the "paper supplier" and nothing more. Consequently, the prospect of a Chinese security footprint in the region appeared to have been greatly diminished.

However, it appears that beyond the damage to China's geo-strategic image in the region, primarily among commentators, China's relations with Middle Eastern states during 2025 did not in fact undergo a retreat and, at times, quite the opposite. This is evident when examining the following dimensions: trade; technological ties, investment and finance; security relations; and high-level official visits. Furthermore, this paper contends that, for certain states in the region, such as Egypt, the development of relations was even more profound. This does not suggest that China has altered the overall trajectory of its relations in the region. Rather, China has continued to reinforce longstanding trends in these relations, particularly in the economic sphere, while remaining weak in other aspects, especially foreign policy and security.

Trade

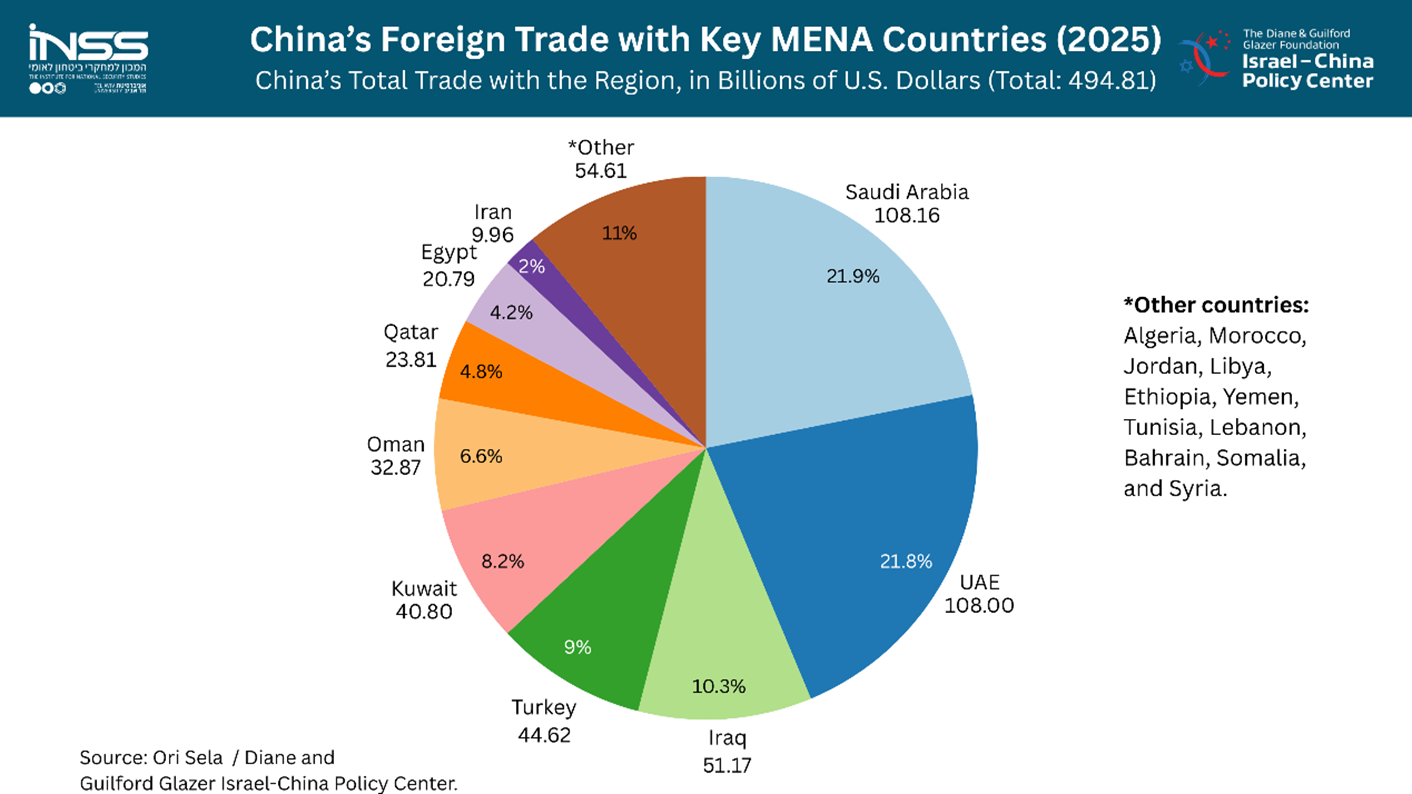

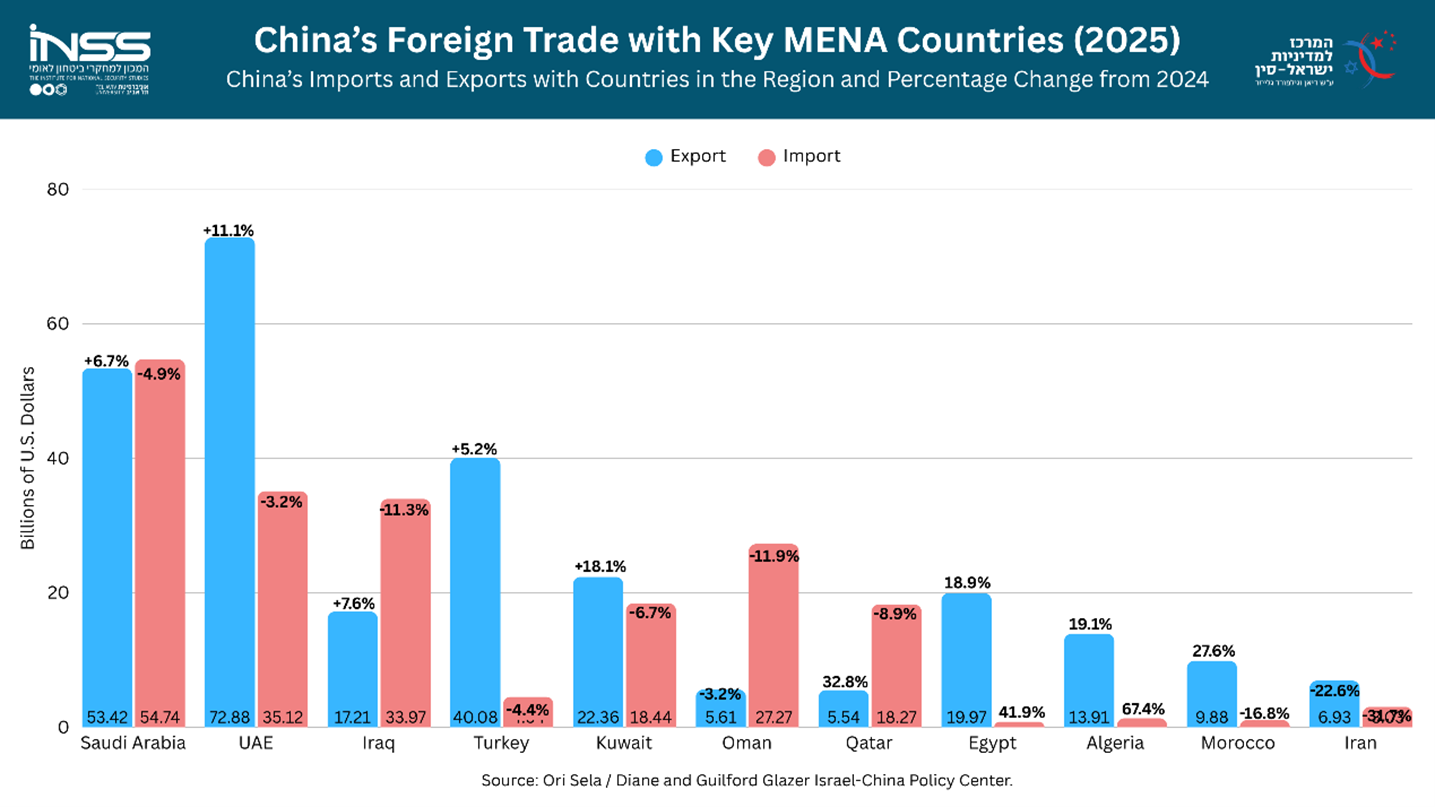

Trade data between China and selected countries in the Middle East and Africa in 2025 indicate, according to Chinese customs figures, a distinct increase in Chinese exports compared to 2024 in nearly every country in the region: $293.5 billion, an increase of more than 10% from the previous year. Although exports to Iran declined according to the official data, these figures do not account for the import of Iranian oil, which continued to flow to China at an average rate of approximately 800,000 barrels per day throughout 2025. Conversely, Chinese imports from the region plummeted to approximately $201 billion, a decline of about 7.5%.

China’s two principal trade partners in the region remained, as in previous years, Saudi Arabia and the United Arab Emirates, each with a trade volume of approximately $108 billion. Trade with the UAE increased by 6%, while trade with Saudi Arabia remained nearly unchanged. Following these were Iraq ($51 billion), Turkey ($44 billion), Kuwait ($40 billion), Oman ($33 billion), Bahrain ($30 billion), Egypt ($21 billion), and Qatar ($23 billion).

Trade volumes declined with Iraq, Oman, and Qatar, while increasing with Bahrain, Egypt, and Turkey. In most cases, even where overall trade volumes increased, the broader trend of declining imports into China alongside rising Chinese exports remained pronounced both in the Middle East and beyond. Notably, Egypt, Algeria, Bahrain, and Ethiopia recorded impressive growth in their exports to China.

Still, total trade with these countries rose by approximately 2.5% in 2025, reaching roughly $495 billion. This compares with trade volumes of $1.05 trillion with ASEAN nations, $828 billion with all member states of the European Union, $559 billion with the United States, and approximately $549 billion with all Latin American countries. If China’s trade with the region is calculated to include Israel as well, based on data from the Israel Central Bureau of Statistics (CBS), the total volume surpasses the half-trillion-dollar mark, reaching approximately $517 billion.

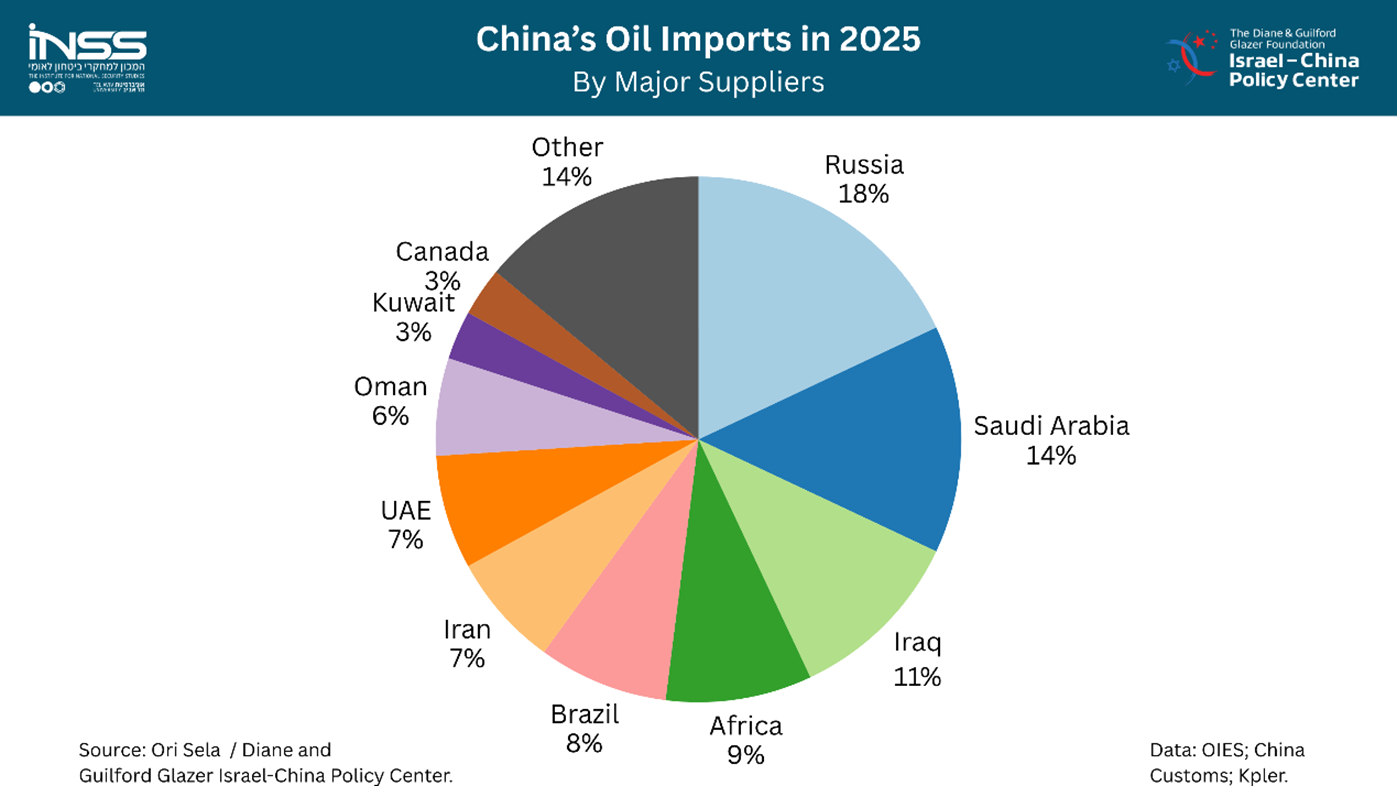

While energy (primarily oil from the Gulf states and gas from Qatar) continues to constitute a significant share of Chinese imports (nearly half of China's energy imports originate in the Middle East, including Iran), and traditional industrial goods ranging from textiles to industrial machinery continue to comprise the bulk of Chinese exports to the Middle East, the share of newer products expanded throughout 2025, continuing a trend seen in recent years. For example, the share of electric vehicles, buses, and rail equipment (including railcars and locomotives) in Chinese exports to various countries has continued to grow, accounting for as much as one-fifth of exports to countries including Egypt and Turkey. More broadly, China remained the leading exporter to the vast majority of countries in the region, even if it was not necessarily their primary export destination.

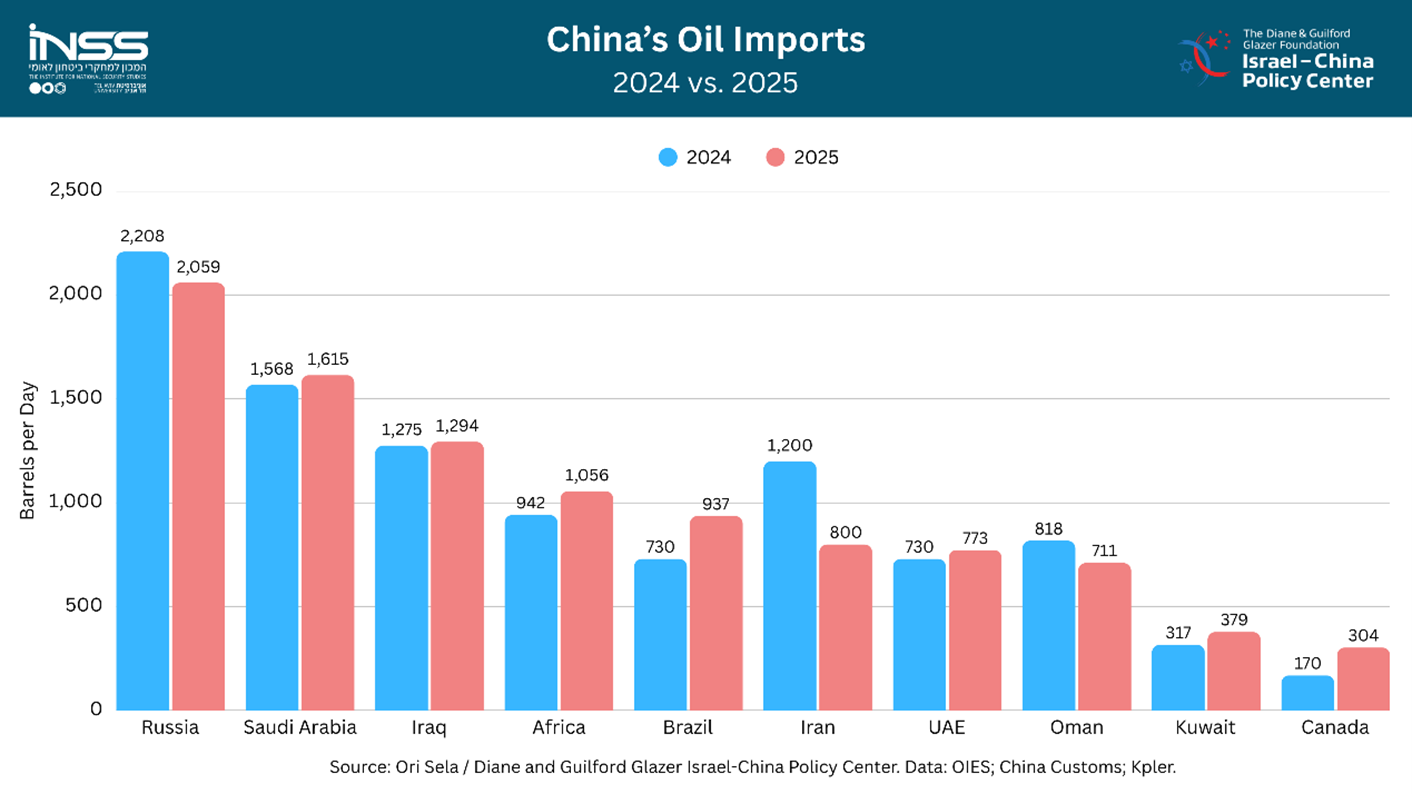

Iran constitutes an exception, with the volume of Chinese trade declining by more than a quarter, both in Chinese exports to Iran (a decline of approximately 32%) and Chinese imports from Iran (roughly 23%). This occurred alongside the continued export of Iranian oil to China, totaling billions of dollars, which is naturally not reported in official Chinese customs data. According to estimates, Iran sold an average of approximately 800,000 barrels of oil per day to China throughout 2025, at prices ranging between $60 and $70 per barrel. In total, this amounts to more than $20 billion over the course of 2025. This volume accounted for more than 80% of Iran’s oil exports and approximately 7% of total Chinese oil imports for that year.[1]

Technological Ties, Investment, and Finance

Trade, of course, is not the sole metric for assessing the depth relations between states. Ties in the technology sector, particularly as manifested in investments and joint financial ties, serve as another indicator of China's relations with Middle Eastern nations. This refers not only to Chinese investments in the region, but also to investments by regional states in China or in Chinese companies. In this regard as well, one can observe stability and even growth, although investment data remain preliminary at this stage and will only be fully published later on.

In January 2026, in a preliminary report on foreign investment in China, the United Arab Emirates stood out with a significant 27.3% increase in investments in China (compared to 2024). Based on past trends, it may be cautiously estimated that this amounted to approximately $2–3 billion in direct investment from the UAE in China itself.

However, specific investment and financial agreements jointly involving China and countries in the region were explicitly announced throughout 2025. These agreements and contracts cover a broad range of sectors: from traditional and green energy to water desalination, manufacturing plant construction, and infrastructure development. They also include agreements regarding payments in local currencies and the yuan. Within these frameworks, alongside the dominance of Saudi Arabia and the United Arab Emirates, a wide range of other regional states is also represented.

In parallel, space-related ties between China and countries in the Middle East and Africa continued to deepen throughout 2025. While comprehensive data on specific deals and investments is not yet fully available, even the partial and preliminary figures suggest these relations have remained stable at the very least, despite the significant shadow cast by President Trump over the region. At the same time, developments in sensitive technological fields such as Artificial Intelligence (AI) warrant close monitoring to determine if cooperation with China will in fact decline, particularly with countries like Saudi Arabia and the United Arab Emirates. In other words, the question is whether, in the near future, the Gulf states will deepen cooperation with the United States on issues involving the most advanced and sensitive technologies (such as civilian nuclear energy and data centers), while continuing or even expanding cooperation with China in fields involving advanced but somewhat less sensitive technologies.

Reports of Alibaba Cloud (the digital technology and artificial intelligence division of Alibaba Group) opening a second data center in Dubai (without disclosing an exact investment amount at this stage), further complicate this issue. These reports are linked to the company’s public commitment to invest $53 billion over three years in the United Arab Emirates.

Security Ties

Throughout 2025, as in previous years, reports surfaced from time to time regarding emerging arms deals between China and Middle Eastern states. This year, Egypt took center stage amid a range of reports (some recycled from earlier periods) concerning the acquisition of Chinese weapon systems, ranging from advanced surface-to-air missiles (HQ-9B) to J-10C fighter aircraft. All of these reports remained unverified and, at this stage, appear to lack any substantive basis.

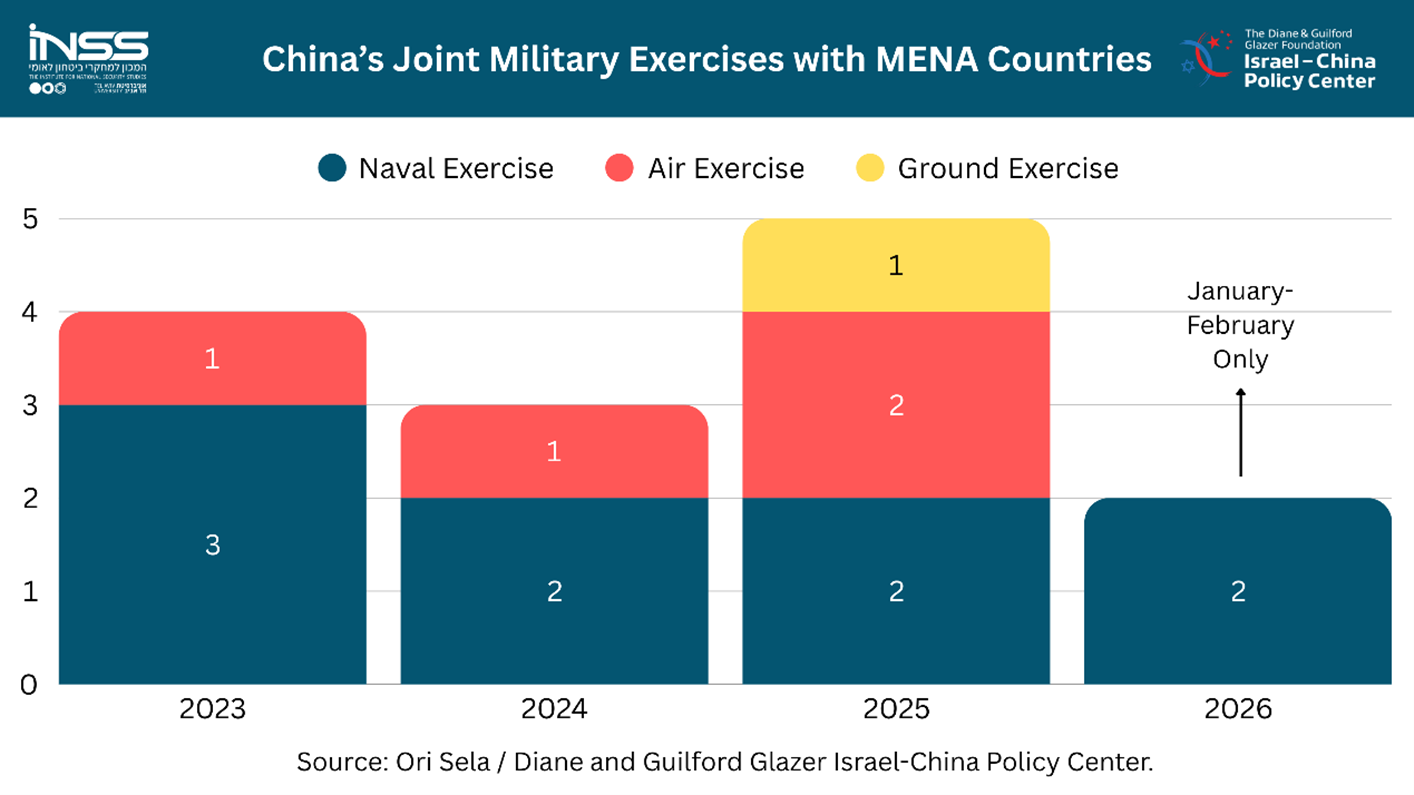

China's security footprint in the region remained minor, consisting primarily of the naval anti-piracy task force, which continued its operations throughout the year. With regard to arms supplies to Iran, in the period leading up to and following the 12-Day War with Israel in June 2025, numerous unverified reports circulated concerning the sale of air defense batteries, fighter aircraft, and radar systems. At the same time, China continued to supply materials that could potentially support Iran’s missile program, and likely also certain components for Iranian weapons systems, though not complete Chinese-made weapons systems. Alongside this, it is entirely possible that China has been sharing intelligence with Iran.

However, in 2025 China expanded its joint military exercises with countries across the region. While the vast majority of the naval drills involved Chinese Navy vessels already present in the area as part of China’s anti-piracy task force, it is still evident that the nature of these exercises shifted over the past year. The scope of the drills increased, spanning maritime, ground, counterterrorism, and aerial arenas, while their linkage to international frameworks led by China (SCO, BRICS) became more pronounced. Additionally, China continued to deploy forces to UN peacekeeping missions in South Sudan and Lebanon.

Senior-Level Visits

In 2025, a cautious yet consistent deepening of China's involvement in the Middle East, North Africa, and East Africa was evident, with an emphasis on diplomacy rather than formal alliances. The pattern of visits indicates a clear preference for state-ministerial channels (primarily foreign ministers and vice presidents) rather than heads of state, allowing Beijing political flexibility and risk mitigation.

The central issues discussed—the Gaza Strip and regional stability, energy, investment, and the Belt and Road Initiative—reflected China's aspiration to position itself as a stabilizing economic force without becoming entangled in conflicts. Simultaneously, China maintained a balance between rival actors (Iran and the Gulf States, Turkey and the West) and deepened its presence in East Africa through debt and development frameworks. Overall, 2025 reinforced China's image as a mediating and economic power rather than a designer of regional security order.

In quantitative terms, the number of senior-level visits in 2025 reached approximately 25–30 reciprocal visits, compared to only 15–20 in 2024, reflecting an increase of about 40–60%. In 2024, most visits were one-off engagements conducted at the foreign minister level or below, aimed primarily at managing specific crises, especially those surrounding the war in Gaza and its regional implications. By contrast, 2025 saw both an increase and intensification in diplomatic exchanges, including repeated visits to the same key capitals (Cairo, Riyadh, and Tehran) alongside a rise in visits conducted at the level of vice presidents and prime ministers. Furthermore, 2025 demonstrated greater symmetry between outgoing and incoming visits (roughly a 1:1 ratio), whereas in 2024, the relationship leaned toward unilateral Chinese initiatives. Overall, the transition from 2024 to 2025 reflects a quantitative and qualitative upgrade in engagement, while carefully avoiding formal alliances. While the increase in senior-level visits could be interpreted as a sign of weakness and an effort by China to bolster its regional standing, the sharp rise in visits by regional officials to China suggests that regional players are no less interested in strengthening ties with China than China is in deepening its engagement in the region.

Another Great Power Competition: India

While the principal great power competition most commonly discussed is that between China and the United States, the Middle East (and elsewhere) is also witnessing a growing rivalry between China and India. For instance, trade between India and the Gulf states alone reached approximately $180 billion in the 2024–2025 fiscal year (according to Indian trade reports). In fact, over the past five years, this trade has grown by an average of about 15% annually, accompanied by the signing of economic and technological agreements between various Middle Eastern countries and India. The UAE stands out as India's most significant trade partner (totaling approximately $100 billion), followed by Saudi Arabia with more than $40 billion. Similar to China, India also focuses on energy imports as the dominant commodity from the region.

India’s prime minister has visited the United Arab Emirates seven times over the past decade, most recently in 2024, while the ruler of the UAE has himself visited India several times, most recently in January 2026. India’s foreign minister visited the UAE twice during 2025, in January and December, underscoring India’s strategic interest in both the country and the broader region.

In December 2025, India’s prime minister also visited Oman, Jordan, and Ethiopia. Collectively, these visits signal the strengthening of ties between India and regional states, where millions of Indian citizens live and work. During these visits, a range of agreements were signed to expand trade and technological cooperation, further positioning India as a significant competitor to China in overlapping areas of interest.

Furthermore, China does not operate in the Middle East solely against the backdrop of great power competition—that is, external competition involving the United States, India, and to some extent Russia—but also within the context of intra-Middle Eastern tensions and rivalries. This includes inter-Arab competition, such as that between the UAE and Saudi Arabia, or the friction between both of them and Iran. In this state of affairs, China is required to navigate carefully and attempt to maintain an agenda that reflects its interests: being "everyone's friend."

Conclusion and Implications for Israel

Against the backdrop of China’s significant regional ties, the broad range of Chinese statements in various forums (from the United Nations and the Security Council to bilateral meetings) on political and diplomatic issues, and its efforts since March 2023 to position itself as a regional mediator (most notably through the Iran–Saudi Arabia agreement, which did not hold up well in the 2026 war), one fact stands out: China remained largely irrelevant to the major conflicts that shook the Middle East throughout 2025. This is even more pronounced in light of President Trump’s activism, which yielded tangible diplomatic, economic, technological, and security-related results.

China, therefore, continued to strengthen or maintain its traditional areas of engagement (trade, economy) while remaining marginal in terms of substantive foreign policy and security (geo-strategy), even as it intensified its civilian and military diplomacy (exercises, visits). The question of advanced technology cooperation, however, remains unresolved at this stage.

In other words, Andrew Scobell’s assessment from the previous decade—that China in the Middle East is “an economic heavyweight... a diplomatic lightweight and... a military featherweight”—remains largely valid, despite all the regional shifts that have taken place over the decade since those words were written in 2015. Even the growing pace of military exercises with regional states appears more like an extension of Chinese diplomacy, aimed at image-building rather than operational utility, conducted through military means rather than a move to significantly increase China’s military footprint in the region. Nevertheless, for China, extensive and expanding economic ties also mean increased exposure and risk, especially in times of crisis and instability.

Israel fits well within the broader framework of China–Middle East relations described above in 2025. Here too, despite Israel’s close ties with Washington and the strong relationship between Prime Minister Benjamin Netanyahu and President Trump, 2025 marked a record high for trade in goods between Israel and China, with an increase of approximately 8% compared to 2024. In the Israeli context as well, the bulk of this trade growth stemmed from an increase in imports from China; out of the total trade (which stood at $21.716 billion), Israeli exports to China accounted for only about one-fifth ($4.233 billion).

While Israel had grown accustomed to a cold and hostile attitude from China since October 2023, it appears that following Israeli successes in the war in Lebanon in 2024 and against Iran in the summer of 2025, the year 2025 signaled a certain positive trend in China's stance toward Israel. Alongside condemnations, particularly in international forums such as the UN and the Security Council, there are noticeable attempts to improve relations, once again primarily in the economic-business sphere.

Nevertheless, from Israel's perspective, China has not become a significant factor in a diplomatic or military context. Unlike many other countries in the region, reciprocal high-level visits between the two sides have yet to materialize. This remains the case despite various media statements suggesting that both sides are interested in stabilizing and improving relations, even in the shadow of significant geopolitical disagreements.

In this regard, Israel—particularly since the war with Iran in June 2025 and certainly throughout the joint Israel-U.S. campaign against Iran in 2026—is also perceived by China as a regional destabilizer and a state aspiring to regional hegemony. These are two deeply problematic traits in the eyes of China, and may carry future implications for bilateral relations.

From the standpoint of Israel's economic needs, it would therefore be wise to continue advancing commercial cooperation, provided it is done while managing national security risks and tempering expectations regarding which fields remain relevant. This must be weighed both against the backdrop of great power competition and China’s ties with Israel’s regional adversaries, chief among them Iran.

Furthermore, it is vital to recognize that massive American involvement in the Middle East does not signal a decline in Chinese engagement. On the contrary, it indicates an intensification of great power competition in the region. As seen in the past, this dynamic will likely impact Israel’s ability to maneuver between Washington and Beijing, yet it may also open new avenues for regional collaborations that leverage this very competition.

Concluding Note: China and the 2026 War in Iran

In the war between Israel and the United States against Iran, China persisted with the same policy line that characterized its conduct during the 12-Day War in June 2025. That is to say, its support for Iran remained minor, both on a diplomatic-declarative level and in practical terms. Although Beijing, as in the past, focused on condemning Israel and the United States, it did not go beyond that.

For example, in mid-March, China abstained from a Security Council vote on a resolution condemning Iran, rather than exercising its veto, thereby allowing the resolution to pass together with Russia. In practical military terms, there was little evidence of substantial Chinese assistance, though reports resurfaced regarding the supply of materials for Iran's missile program, information and intelligence support, and later—following the onset of the ceasefire—reports of a potential supply of air defense systems. Some of these reports were denied by China and remained unverified by other sources. Furthermore, in early April, China and Russia vetoed a different Security Council draft resolution concerning the Strait of Hormuz, just one day before the ceasefire took effect on April 8.

Simultaneously, China continued to emphasize its opposition to any attempt to "interfere in the internal affairs" of Iran (or any other state), and it appears its preference is for the war to end without the collapse of the Iranian regime. Even in a regime change scenario, China assesses that it could benefit from any future easing of sanctions, should any occur, as well as from the profits of post-war reconstruction.

By contrast, a scenario of chaos in Iran is particularly troubling to Beijing, not only because of its commercial implications, but primarily due to a fear of terrorism leaking into China itself via Central Asia and Afghanistan/Pakistan. Furthermore, China fears the potential destabilization of countries it considers more vital to its interests, foremost among them Saudi Arabia and the United Arab Emirates.

In the energy sphere, this does not yet constitute a severe crisis for China, thanks in part to the diversification of its oil sources and the buildup of reserves in recent years—including the purchase of discounted oil from Russia, Iran, and Venezuela. However, as the war dragged on, or should the ceasefire collapse, price hikes and disruptions to maritime shipping routes could exacerbate the damage. At the same time, China’s relative dependence on natural gas imports from Qatar highlights a structural vulnerability: beyond the economic implications, it diminishes China's ability to exert economic or diplomatic pressure on other suppliers, such as Australia.

The war also carries broader macroeconomic implications for China. Rising energy prices and supply disruptions affect the Chinese economy both directly, through higher energy costs, and indirectly, through increased production costs, weaker external demand, and supply chain interruptions. These trends complicate Beijing’s efforts to strengthen domestic consumption and weigh on overall economic growth. One particularly affected sector has been the fertilizer industry, which depends heavily on natural gas, creating consequences for agriculture as well. China is taking countermeasures, subsidizing fuel prices, restricting fertilizer exports, and advancing energy reforms, but in the short term, it bears a share of the economic costs of the war. Even so, the relative impact on China remains moderate compared to other East Asian nations that are more heavily dependent on Gulf oil, such as Japan, and certainly less than the United States, which bears the primary burden of financing the war.

From China’s perspective, the war reinforces the narrative that the United States is a “warmonger,” while China works toward stability and peace. Accordingly, Beijing assesses that its relatively neutral stance (from its own perspective, of course) may actually strengthen its regional standing over the long term. This is a gamble, but one with limited potential costs, partly due to the already low expectations among regional states for Chinese security involvement.

China assumes that its lukewarm response to Iranian aggression against its partners will not damage its relations with them, as those ties are rooted primarily in economic interests. The perception of Israel as a destabilizing actor aspiring to regional hegemony has actually intensified; from Beijing's standpoint—to the extent that regional states share it—this perception may even strengthen China's ties with them after the war.

Beyond this, China may seek to deepen economic, diplomatic, and technological ties, and possibly even expand arms exports, albeit still on a limited scale. The fact that the Crown Prince of Abu Dhabi visited Beijing shortly after the ceasefire was announced, alongside a call between the Chinese President and the Saudi Crown Prince, without similar senior-level moves involving Iran, underscores which states remain China's primary interests in the region.

Finally, within the broader context of East Asia and the Indo-Pacific, any depletion of American resources—whether through the diversion of forces or the expenditure of munitions in this arena—is viewed positively by China. Against this backdrop, President Trump’s planned visit to China in May may carry particular significance, both in relation to the war and within the broader relationship between the two powers. In this context, Beijing may attempt to leverage its involvement in the Middle East to secure American concessions, including the Taiwan issue. Even the reports, at times exaggerated, regarding Chinese mediation efforts surrounding the ceasefire and its potential role as a guarantor contribute, from its perspective, to strengthening its standing and bargaining power in the international arena.

The main question that remains open at this stage is whether and how China will be involved in Iran's reconstruction, specifically in rebuilding the various dimensions of Iran’s military industry following the war. Israel must act in the international arena, not only through military and intelligence channels, in an effort to influence China. In collaboration with other regional nations that were also targeted by Iran, Israel should aim to influence Beijing to refrain from such involvement, particularly regarding the restoration of Iran's military capabilities.

Another question arising from the war is whether China's model of engagement—economic power without corresponding security responsibility—can endure over time under conditions of ongoing regional escalation. The intensifying great power competition may shift its characteristics as a result, and Israel must prepare for this in advance.

____________________

[1] Estimates regarding Chinese oil imports from Iran often present significantly higher figures, for example, 1.3 million barrels per day. However, these higher estimates appear to be based on isolated peak periods, whereas the annual average, despite such spikes, seems to have stood at approximately 800,000 barrels per day over the course of the year as a whole. For a comprehensive review of the issue, based on both Chinese customs data and research by Kpler and OIES, see: Michal Meidan, 2026, Disruption in the Strait of Hormuz: Implications for China’s Energy Markets and Policies. The Oxford Institute for Energy Studies. https://www.oxfordenergy.org/wpcms/wp-content/uploads/2026/03/Comment-Turmoil-in-the-Middle-East.pdf