Publications

What are the main characteristics of the budget approved by the government, and why does it fail to meet the broader economic needs of the country or provide a reason for credit rating agencies to reverse their decision to downgrade Israel’s credit rating?

INSS Insight No. 1919, December 2, 2024

Follow us on GoogleThe 2025 state budget, set at NIS 607 billion, was approved by the government on November 1 after contentious debates within the coalition. The government aimed to present a budget that would support the country’s growing security needs and the populations affected by the war while also reducing the deficit and encouraging economic growth. In practice, the approved budget should meet Israel’s security needs, but it is doubtful whether it will address the country’s broader economic needs. The unwillingness to significantly cut coalition spending, close unnecessary ministries, and provide support for economic growth engines, in addition to the adverse effects on the working population, all cast great doubt on the state’s ability to meet the growth forecast of nearly 4.5% in the coming year as announced by the Ministry of Finance. Moreover, the government’s economic conduct has confirmed the concerns of the credit rating agencies, which have downgraded Israel’s rating several times in the past year and are warning of the risk of a financial crisis.

The state budget for 2025 was planned against the backdrop of one year since the beginning of the war in Gaza, which has taken a considerable toll on the local economy, as shown by several metrics. First, the annual deficit in September 2024 exceeded the planned deficit by almost 2 percentage points, reaching 8.5% of GDP, compared to just 1.5% a year earlier. Second, growth has been severely affected. In 2023, growth was only 2%—resulting in negative growth per capita of 0.1% given the high population growth in Israel. The growth forecast for 2024 is only 1%, which would lead to negative 1% growth per capita. Third, about 59,000 businesses have closed in Israel since the war began, while 36,000 new businesses have opened. In a regular year, about 50,000 new businesses open and 40,000 shut down. If not for governmental support, the damage to businesses could have been much worse, but the costs are still likely to be felt in the coming years. In addition, the war continues in multiple arenas, with varying intensity, and it is not clear when it will end; the cumulative burden on the reserve soldiers and their families is also increasing, as are the security challenges.

In this context, the budget planning was more difficult than in previous years. The government’s stated aim on the eve of the budget’s approval was to create a budget that would address growing security challenges while helping to maintain the country’s economic resilience. However, an examination of the approved budget casts great doubt on the government’s ability to achieve this goal.

The Budget Approved by the Government: Main Characteristics

The new budget of NIS 607 billion reflects an increase of NIS 20 billion from the 2024 budget of NIS 587 billion and a significant rise of NIS 100 billion over the original 2024 budget approved before the war started. This increase in the budget reflects the high costs of waging the current war. Consequently, the defense budget for 2025 will be NIS 117 billion, despite the Ministry of Finance’s opposition to such a large budget. On the eve of the budget’s approval, the Ministry of Defense and the Ministry of Finance reached an agreement on a defense budget of NIS 102 billion. In practice, however, the government approved a budget that is 14% higher and comparable to the defense budget of 2024. Furthermore, this increase was approved before receiving the recommendations from the Commission to Examine the Defense Budget (the Nagel Commission), which is expected to recommend an additional increase in the defense budget, likely financed by increasing the budget deficit. In comparison, the 2024 defense budget that was approved before the war was only NIS 65 billion.

Aside from the defense budget, which includes direct expenses for the war effort, the impact of the war is reflected in various items in the current budget, such as NIS 15 billion for a five-year plan to rehabilitate and develop northern Israel, NIS 5 billion for the Tkuma program, aimed at rehabilitating the communities of the Western Negev, and other programs intended to compensate victims of the war. These expenses are necessary, but, of course, the funding for the budget will not appear out of nowhere and will force the government to cut its expenses while increasing the tax burden on the public.

The state budget was an excellent opportunity for the government to “help carry the burden” and lead by example the participation in the war effort. However, in practice, the government missed this opportunity, with most of the burden falling on the working population. The most conspicuous measures imposed include raising the National Insurance and health taxes, increasing the VAT to 18 percent, and freezing income tax brackets, which will increase tax payments for workers. All these measures will be strongly felt in the coming year, especially among the middle class. In contrast, many considerations related to maintaining the governing coalition prevented additional cuts. For example, the size of the coalition funds will be NIS 5.4 billion, compared to the NIS 4.1 billion outlined in the proposed budget, including over NIS 600 million in support for private schools that do not teach the core curriculum. In addition, despite calls since the beginning of the war to close government ministries, not a single ministry has been shut down. The Arrangements Law had proposed closing five government ministries, and in December 2023, the professional echelon in the Ministry of Finance suggested closing ten unnecessary ministries. In practice, due to coalition considerations, no government ministry will be cut, even though the cost of each is estimated at hundreds of millions of shekels. It is important to note that closing government ministries and dramatically cutting coalition funds will not solve the budgetary problem for the coming year, but it would have had symbolic value by setting an example for the nation, which has been suffering the economic consequences of the war for over a year.

Ultimately, the 2025 budget has two prominent characteristics:

- The deficit target for the 2025 fiscal year increased above 4%, over the threshold that Finance Minister Bezalel Smotrich promised. The deficit target is expected to exceed 5% after the adoption of the Nagel Commission’s recommendations and its approval process in the Knesset.

- The current budget does not include significant economic reforms or other measures to support future growth engines.

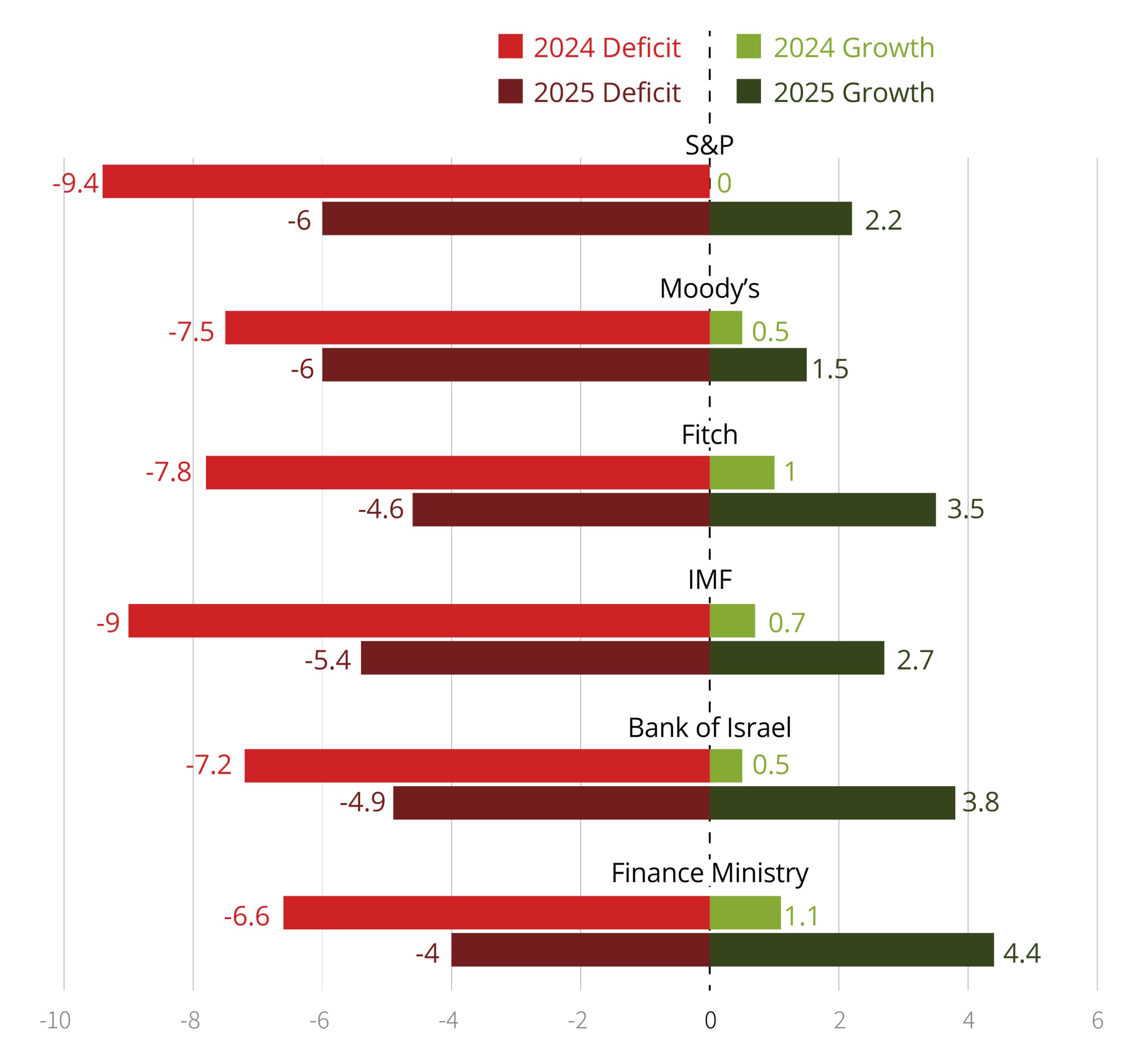

Therefore, as we can see in Figure 1, there is general agreement in the forecasts by the Ministry of Finance, the Bank of Israel, the International Monetary Fund, and the credit rating agencies, that next year the Israeli economy will suffer from a high deficit and relatively low economic growth. Furthermore, Figure 1 shows that Israeli institutions tend to be more optimistic than international institutions. It should be noted that since the war began, the forecasts of international institutions have proven to be more accurate.

Figure 1. Israel’s Deficit and Growth Forecasts by Various Organizations

Heading Toward a Financial Crisis?

The government has so far financed the economic cost of the war by increasing the debt. As a result, Israel’s debt-to-GDP ratio is significantly rising and is now approaching 70%. The risk premium on Israeli government bonds is also increasing and has exceeded 1.7%, compared to just 0.8% before the war. (The risk premium measures the yield gap between government bonds issued in dollars and US 10-year Treasury bonds.) Israel’s current risk premium is similar to that of Romania and higher than that of countries like Peru, Mexico, and Hungary. It is therefore not surprising that all credit rating agencies have downgraded Israel’s rating over the past year and issued negative forecasts for the Israeli economy. Moody’s downgraded Israel’s rating by three levels, S&P by two, and Fitch by one. Israel’s credit rating is now alarmingly close to “junk” status. Reaching that level would prevent many institutional investors from buying Israeli government bonds and even bonds issued by Israeli companies.

The credit rating agencies will continue to scrutinize Israel’s economic policies in the coming year. In their reports, they have already noted the ongoing war that does not have an exit strategy, the social polarization, and the current government’s irresponsible economic conduct as key reasons for an increase in the economic risk of investing in Israel. They have all stated that Israel’s deficit will be higher than what the Ministry of Finance predicts and are expecting a deficit of up to 6% in 2025 (see Figure 1).

To mitigate these concerns, the government should approve a responsible 2025 budget that clearly demonstrates its commitment to addressing Israel's economic challenges. Otherwise, the risk of Israel suffering from a financial crisis in the coming years will increase. Israel already experienced such a crisis at the height of the Second Intifada. In this scenario, investors lose confidence in the country’s ability to repay its debts, the risk premium soars, and the government is unable to finance its expenses by increasing the debt. A financial crisis would lead to a fiscal crisis, resulting in a deep recession. Such events would not only harm the country’s economic resilience but also the entire war effort. It is difficult to imagine a situation in which the State of Israel maintains military operational freedom while its economy collapses.

The budget is expected to be approved by the Knesset in late January. This provides sufficient time for the government to make necessary adjustments at the recommendation of the Ministry of Finance. Meeting a deficit target of 4%, closing government ministries, cutting coalition funds, and providing broad support for growth engines are a small set of recommendations that could improve Israel’s economic situation. A strong and stable economy is critical to Israel’s national security in peacetime, and even more so in wartime.