Strategic Assessment

The Chinese government recently announced that rare minerals are a national asset, and that organizations and individuals are prohibited from taking control of such resources. The announcement was accompanied by the introduction of a program to track and control all the rare mineral resources at China’s disposal, including their production, processing and export. The announcement links to the fact that the Chinese regime, which is striving for political and financial dominance largely because of its internal needs but also due to its global vision, has identified the decisive importance of the market for metals and minerals—including nickel, copper, cobalt, magnesium, rare earths metals and rare ores and as well as others —for both the Chinese and the global economy, and as an engine of growth in the twenty-first century.

The importance of minerals, including rare earth elements, lies primarily in their uses for green energy, the electric vehicle industry, electronic products, medicine, lasers, optical fibers, magnets in the motor industry, various aspects of the security industry, and the global microchip industry. These minerals are the building blocks for all branches of modern industry, and therefore control of their chain of supply is essential for the economic development of China itself, as well as a means to position China as an important player in the global economy, with considerable capabilities that can be leveraged for political influence. Over the past thirty years, China has made huge investments in mines and plants that process and refine critical minerals in Africa, and in some markets it has absolute dominance, up to 90 percent in the case of certain products. This fact has economic and political implications, particularly for China’s relations with the United States, and with countries in Africa, Europe, Asia and Southeast Asia.

Israel’s knowledge-intensive industries (hi-tech) and its security industry must limit their exposure to the risk of a global shortage or political or economic restrictions on the imports of special critical minerals, by developing confidential contacts and partnerships in countries with the relevant natural resources in Europe and in Africa.

Keywords: minerals, metals, rare earth elements, lithium, antimony, magnesium, electric vehicles

Introduction

The metals and minerals market are critical factors in the global economy, since these metals have unique properties that make them essential in various branches of industry worldwide. This fact is true for both traditional industries, which rely on strong and heat-resistant metal products, and for high tech industries in the civilian and the security sectors based on microchips, an essential component in most modern industrial products. Some rare metals have unique properties that are essential to the function of microchips, but a country that wishes to control the metals and minerals market must also control not only the mining sites but also the technologies for their purification, separation and processing. These metals are natural minerals found deep in the earth, which must be extracted in dedicated mines or by drilling in deep quarries. They are not found in a pure state but in mixtures or chemical compounds, requiring specialized factories and the use of chemical and physical processes that are hazardous to workers and the environment, for their production, purification and separation. For these reasons, it is vital for every country with an interest in these metals and minerals to have some control of their sources, particularly those required for the production of consumer goods, such as iron, copper, platinum, gold, magnesium, lead, cobalt, lithium and derivatives of these compounds, as well as the rare metals professionally referred to as “rare earth elements.”

Background

More than four decades ago the Chinese government identified the importance of the minerals market for the country’s internal needs and economic development, and also as a political means to control certain consumer industries, such as electric vehicles and communications. It aimed to strengthen its economy by stockpiling strategic quantities of these resources. China’s dominance in this field has the potential to create global shortages of products essential to the automobile and microchip industries, magnets for engines and various sensors, giving it economic and military superiority.

Africa is home to 30 percent of the metals and minerals critical for modern industry, and China has gradually taken over mines with practical potential all over Africa. Chinese intervention in Nigeria, for example, is accompanied by investments of some three billion dollars in infrastructure as a lever for economic development, creating 4,000 jobs and tax revenues of 125 million dollars.

The Chinese are acquiring control of critical metals and minerals infrastructure in African countries—mines and raw material processing factories—without imposing financial or political conditions, together with investments in the development of additional civilian infrastructure such as railways, which in future could be used to transport goods of importance to the Chinese government. Such control of the minerals market in Africa and investment in infrastructure, reflects China’s aims of establishing its geostrategic status as a leading power, both politically and economically, while creating mutually beneficial partnerships. The process largely consists of investments in cobalt and copper mines in Congo and Zambia, and lithium mines in Zimbabwe, as well as in rare earth element mines. It is accompanied by massive monetary investments while exploiting workers and ignoring extensive environmental damage. Control of the rare earth elements market is essential for the development of the next generation of smart chips and advances relating to green energy, such as solar panels and batteries for electric vehicles. Microchips are central components in consumer products of a modern economy—computers and telephones, as well as advanced weapons systems. The Chinese government is well aware of the power afforded by its control of the supply chain of minerals essential to chip production, particularly when the centers of chip production in South Korea (Samsung) and Taiwan (TSMC Ltd.) are located in an environment hostile to China and North Korea. Ironically, although the first microchips were developed in the United States, the American chip industry currently supplies only 10 percent of global consumption, and the country’s reliance on external suppliers is a considerable cause for concern in the US administration.

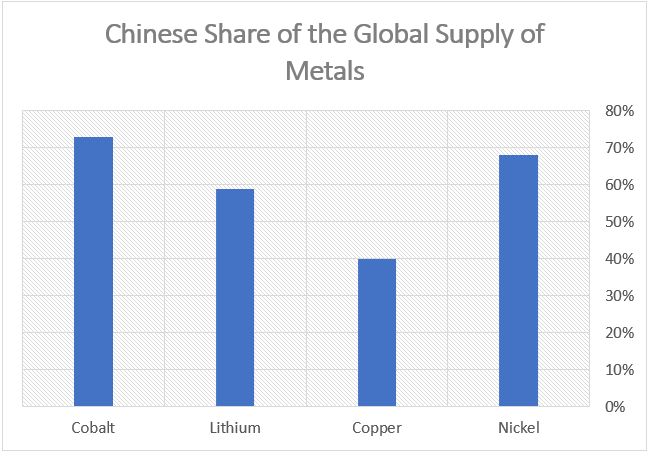

China’s massive investments and dominance of the mining market enable it to regulate the supply and demand of components vital to the production of products forming the cornerstone of a modern economy. Its control of the supply chain of the basic raw materials needed in a wide range of industries has significant geopolitical effects. As of 2022, the Chinese share of global supplies of metals essential to the production of components for various technology industries is shown in the following chart, based on market data:

Chinese investments around the world amounted to about 1.34 trillion dollars in the years 2000-2023. It should be noted that out of this amount, a total of 403.740 billion dollars was channeled into mining and infrastructure construction projects worldwide. 11.3 percent of this amount (45,190 billion dollars) was invested in 224 projects in Africa dealing with the exploitation of various natural resources, such as mining and processing minerals, drilling and producing crude oil and gas.

Chinese Activity in the Field of Critical Minerals

Rare Earth Elements (REE)

REE are metals and minerals that are found in very small quantities deep in the earth. Producing the highly purified minerals required for knowledge-intensive industries is a complex process that can only be done in specialized factories. REE are used mainly in the vehicle industry (catalytic converters, magnets for electric engines), lasers and lighting, and the forecast is for exponential growth in market demand for REE uses. The world’s main REE reserves are estimated at 110 million tons, of which 44 million tons (about 40 percent) are owned by China, although not necessarily located in that country. China has acquired mines and REE refineries and cleaning plants and currently controls some 85-98 percent of the industry associated with REE and the products based on these elements, many of which are imported to China.

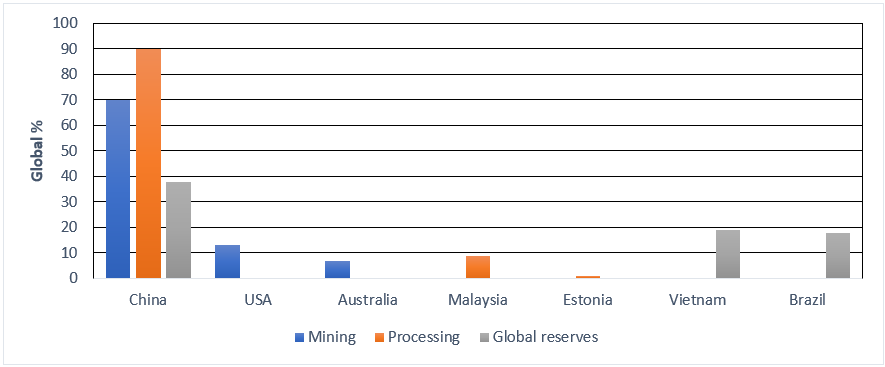

China recognizes the enormous importance of rare earth elements, and therefore recently imposed restrictions on their trade. It is not satisfied with the REE deposits recently discovered within its territory, and is busy accumulating reserves of these minerals through extensive imports from all over the world, in order to dominate the supply chain. The breakdown of the main countries involved in mining, processing and stocking reserves of strategic metals is shown in the following chart, based on the most recently published data:

Recently, the United States and European countries have led a joint technological effort to limit Chinese dominance of the rare earths market, by expanding their purification, cleaning and processing capabilities. The accepted assumption is that by 2030 China will be the world leader in this field, due to its current control of the supply chain and the processes of extraction (60 percent) and processing (90 percent) of rare earths, relative to the five leading countries in this field, which in addition to China are Chile, Indonesia, Congo and Australia.

The Lithium Market

Lithium, which is also known as “white gold,” is an essential component of rechargeable batteries for various applications relating to the production of green energy such as nuclear fusion applications, particularly for use in electric vehicles, mobile computers, cellular communications and solar panels. A further economic benefit of lithium-based batteries is that they can be recycled: The volume of the lithium battery recycling market was 6.5 billion dollars in 2022 and it is expected to reach about 35 billion dollars by 2031, with average annual growth of 20.6 percent. At present the Chinese control the global market for lithium-based batteries; they have completed the construction and upgrade of lithium processing facilities in Zimbabwe and in Mali, and have purchased lithium mines for hundreds of millions of dollars. The total investment by Chinese companies in the acquisition of lithium mines in Zimbabwe and the construction of processing plants for lithium metal in the period 2021-2023 amounted to 1.409 billion dollars. According to the latest figures, the Chinese currently control 65 percent of all the world’s large plants for the processing of raw lithium.

Other Metals

Since the 1980s and 1990s China has made a consistent diplomatic effort to dominate the mining of other metals in Africa, mainly in Zimbabwe, Mali, Ethiopia and Congo. This is because the continent is the source of a considerable proportion of global supplies of critical metals, such as cobalt (70 percent), platinum (90 percent) and manganese (50 percent). Cobalt is critical to the battery industry, and by taking over cobalt mines in Africa, China has become the world’s number one producer of cobalt. China has also acquired control of the global graphite market and currently holds about 90 percent of graphite production in the world, though in order to secure full and lasting control, it imports large quantities of graphite from Mozambique and Madagascar. For purposes of comparison, the United States produces 13 percent of its cobalt consumption and produces no graphite at all, and in the view of the US Administration, this represents a danger to its national security.

The Consequences of Chinese Domination of the Minerals Market

Rare Earth Elements

Control of the critical mineral markets enables the Chinese government to impose trade restrictions and leverage pressure to realize political gains by economic means. For example, in 2010 and 2014 the Chinese tried to force Japan to change its policy towards China by preventing the supply of critical minerals to Japanese industry, causing severe damage to the Japanese automobile industry. During the period 2009-2020, the Chinese government tightened the restrictions on exports of critical minerals to various countries, including a ban on the export of the technologies involved in the extraction and separation of rare earths, an essential element for the semiconductor and microchip industries, with all that entails. For example, the Chinese imposed restrictions on the export of gallium and germanium, rare metals of crucial importance for the global chip industry and the production of fiber optics for broadband communications. Chinese exports of gallium in January-February 2024 amounted to 2,700 kg, compared to 8,800 kg in the same period in 2023. China is responsible for some 60 percent of the global production of these rare metals and controls 90 percent of the factories engaged in processing them. Its actions created a shortage of gallium, causing its price to double to 575 dollars per kg in March 2024.

Lithium

Chinese control of the lithium market has dual significance with regards to essential components for the global vehicle industry: it affects both the chain of supply and the market of lithium for rechargeable batteries for electric vehicles; and it also impacts the supply of microchips needed for computers and processors in new vehicles, including electric ones.

Antimony

The Chinese government recently announced (in August 2024) the imposition of export restrictions on an expensive metal called antimony and its compounds, starting on September 15. Antimony is needed for many security and civilian applications, and China is considered the world’s largest producer of the metal—48 percent of the antimony mined worldwide. These restrictions are in addition to the restrictions that the Chinese government imposed last year on gallium and germanium, both crucial to the microchip industry.

As of 2019 China’s relative share of the global extraction and production of critical metals and minerals ranges from 50 percent for copper and nickel, to 90 percent in the case of REE.

Response from Competitors

It is important to note that Chinese control of various kinds of critical minerals (including but not limited to cobalt, graphite and manganese) is a cause of deep concern in the United States in the context of national security, due to the almost absolute American dependence on imports of essential components from China. The Biden Administration wishes to increase the purchase of critical minerals from countries in Africa, both for reasons of national security, that is, control of the supply chain and reduction of dependence on Chinese imports, and as a geopolitical lever to encourage political stability, accelerate economic development, ease political tensions, and promote government transparency and prosperity in those countries. This is being done largely by bolstering American involvement and the development of infrastructure and business partnerships with countries and companies in Africa. For example, to facilitate its entry into the lithium market in Zimbabwe, the United States recently lifted the sanctions imposed on Zimbabwe and began to invest in civilian infrastructure designed to create a “transport corridor” for the export of lithium through ports in neighboring countries. The US is also investing in local infrastructure and lithium reserves in order to erode the Chinese monopoly in this field and leverage its lithium energy independence for strategic and geopolitical achievements. The US Administration is worried that Chinese control of the market for vital vehicle components is damaging both to its national security and its automobile industry, and indirectly causing environmental damage by raising the price of electrical vehicles, thus encouraging drivers to stick with gasoline-powered vehicles and their high greenhouse gas emissions. Not only that, following rumors of Chinese intentions to purchase lithium, its price rose by six percent compared to early 2024, contrary to the sharp drop in prices in 2022 and 2023.

Chinese control is also a source of concern in Australia and in the European Union, and they are in the process of looking for partners to develop their own technologies and resources in order to strengthen their economies and minimize the Chinese monopoly over various metals and minerals (such as its 94 percent share of total world magnesium exports). Due to the importance of the issue, the EU decided to limit its dependence on external suppliers of critical metals and minerals, including rare earth elements, and to set up a large plant in Estonia. Large deposits of REE were recently discovered in Norway, and—with the combined efforts of the United States, Canada and Australia—a considerable reduction (the report does not specify the quantity) is expected in Chinese control of the REE chain of supply by 2030.

Significance and Recommendations for Israel

Israel must prepare for the possibility of an embargo, including a ban on exports of critical minerals to Israel. In addition to preparing for such a situation, Israel must also be ready for possible global shortages or restrictions on critical minerals, or damage to the chain of supply—events that could deal a fatal blow to its high tech and security industries, and particularly the manufacture of microchips for military and civilian uses. Minerals, certain metals and rare earth elements are vital components of various solid-state devices made in Israel, such as sensors, chips for civilian and military purposes, magnets for engines of all kinds, lasers for medicine and security applications and more. This matter is crucial since Israel manufactures many devices for its own use that it cannot purchase abroad and therefore must have access to the necessary minerals.

The preparations must include first of all a definition of the critical minerals, and a mapping of the essential purposes for which they are required. The supply of critical minerals must be secured by developing confidential ties and partnerships with countries that have natural reserves in Europe, Asia, Africa, the United States, and particularly in South America. Another direction is economic development with the focus on the African continent, investment in infrastructure and generous investments (taking account of Israel’s budgetary constraints) with smaller profit margins in joint ventures in countries with natural resources, similar to China’s current policy in Africa and Israeli activity on the African continent in the 1960s.

Conclusion

Since the early 1980s the Chinese government has been investing in infrastructures used in the mining and processing of minerals in several countries in Africa, such as Congo, Mali, Ethiopia, Zimbabwe and Zambia, as well as investing in civilian infrastructure indirectly linked to this field. Extensive Chinese investments in Africa and elsewhere offer a combined response to both domestic and political-strategic needs. The vision of the combined purpose is the development of the Chinese economy by means of accumulating strategic stocks of critical metals and minerals, or controlling the supply chain of certain consumer goods that are of crucial importance of the Chinese economy and the global economy. This meshes with the vision of Chinese President Xi Jinping, who speaks about controlling the microchip industry (which relies on critical minerals) as an essential component of Chinese national security. In parallel to its efforts to take control of mineral reserves in Africa, the Chinese government is also focusing on developing local natural resources and on massive imports of minerals for processing in China, in order to accumulate large quantities of essential raw materials and thus gain control of the global consumption and supply chain of vital components. The main lesson for Israel is that it must make urgent preparations to handle the risk of a global shortage or restrictions on the import of critical minerals—events that could be fatal to Israel’s high tech and defense industries.