Publications

Recent reports by the IMF and the World Bank emphasized the dismal fiscal situation of the Palestinian Authority, and recommended boosting foreign aid and implementing structural spending reforms. This article proposes an additional policy: a tax on work permits for Palestinians working in the Israeli econony. This measure stands to reduce the Palestinian deficit by one third, and offset some of the adverse effects of employment in Israel.

INSS Insight No. 1611, June 16, 2022

This article proposes a relatively simple policy to help the Palestinian Authority improve its dismal fiscal situation: tax Palestinians who work in Israel and in the Israeli settlements by attaching a fixed price to entry permits, instead of taxing them according to the Israeli/Jordanian tax code. The PA should receive all revenues from this tax. This policy would shift the regulation of the number of Palestinian workers away from an exogenously determined quota to a system that takes into account the supply and demand of Palestinian workers in Israel. A change to the permits system along these lines will lead to several improvements vis-à-vis the current situation.

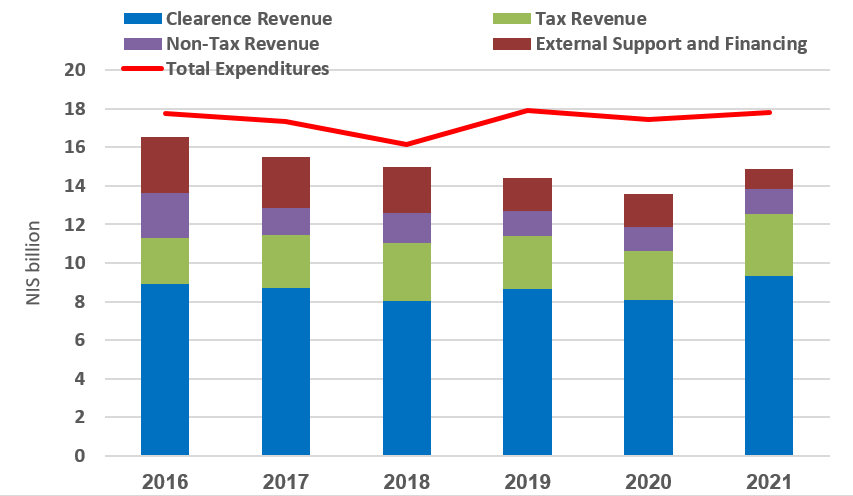

In May 2022 the International Monetary Fund (IMF) and the World Bank published reports with their assessment of the current Palestinian economy, emphasizing the Palestinian Authority’s dismal fiscal situation. Figure 1 charts total expenditures (including development expenditures) and total revenues over the last five years. Whereas expenditures remained fairly constant over time, around NIS 17.5 billion, revenues decreased sharply from NIS 16.6 billion in 2016 to 13.6 billion in 2020, and only partly recovered in 2021 to NIS 14.9 billion. This pattern was dictated by a substantial decrease over time on non-taxed revenues (primarily domestic fees and charges) and on external support from donor countries and organizations. Foreign aid funds decreased by 65 percent, from NIS 2.9 billion in 2016 to one billion NIS in 2021. Thus, in 2021 expenditures are over 15 percent higher than revenues and the fiscal deficit reached 5.3 percent of GDP.

Figure 1: Palestinian Authority’s Revenues, External Support, and Expenditures | Source: Palestinian Ministry of Finance

To relieve this fiscal crisis, the IMF and the World Bank recommend mainly boosting foreign aid and implementing structural spending reforms. This article proposes an additional and relatively simple policy to help the PA deal with this crisis: tax Palestinians working in Israel and in the Israeli settlements.

Palestinian Labor in Israel and Israeli Settlements

The number of Palestinian workers from the West Bank (excluding East Jerusalem) employed in Israel and in Israeli settlements has fluctuated over time. In the first quarter of 2022, after Israel fully recovered from COVID-19, there were about 104,000 documented workers and about 44,000 undocumented workers from the West Bank working in Israel. In addition, by late 2021 Israel renewed the employment of Gazan workers to Israel and established an entry-permit quota of 12,000 workers.

The incentive to work in Israel is clear. Employment to population ratios are extremely low in the West Bank (32 percent when excluding those employed in Israel) and in Gaza (20 percent), compared to 60 percent in Israel. Moreover, there exists a substantial gap between wages in Israel and wages in the West Bank or Gaza. The reported daily wage of a Palestinian worker employed in Israel or in an Israeli settlement equals on average NIS 269. Daily wages for those employed in the West Bank are significantly lower (NIS 126 in the public sector and NIS 118 in the private sector). Workers in the Gaza Strip lucky enough to find a job make 37 percent (NIS 101 in the public sector) or 13 percent (NIS 34 in the private sector) of the average counterpart salary in Israel.

In addition, while workers in the West Bank and the Gaza Strip pay income taxes on their incomes, few workers employed in Israel or in the settlements do so. Palestinians employed in Israel should pay income taxes according to the Israel tax code, and Palestinians employed in settlements should pay income taxes according to the Jordanian tax code. Israel is in charge of collecting these tax payments and transferring them to the Palestinian Authority. In practice, for different reasons, few of these workers pay income tax. The employment of 44,000 undocumented West Bank workers and 12,000 Gaza workers is not official and therefore their income is not reported to the tax authorities. For a large share of documented workers, their incomes are too low compared to Israeli workers and are therefore exempted from paying taxes. In addition, the Israeli tax authorities don’t have strong incentives to enforce the tax laws among these workers since the vast majority of these revenues are transferred to the PA. The bottom line is that in 2021 the PA collected around NIS 250 million from Palestinian workers employed in Israel and the settlements.

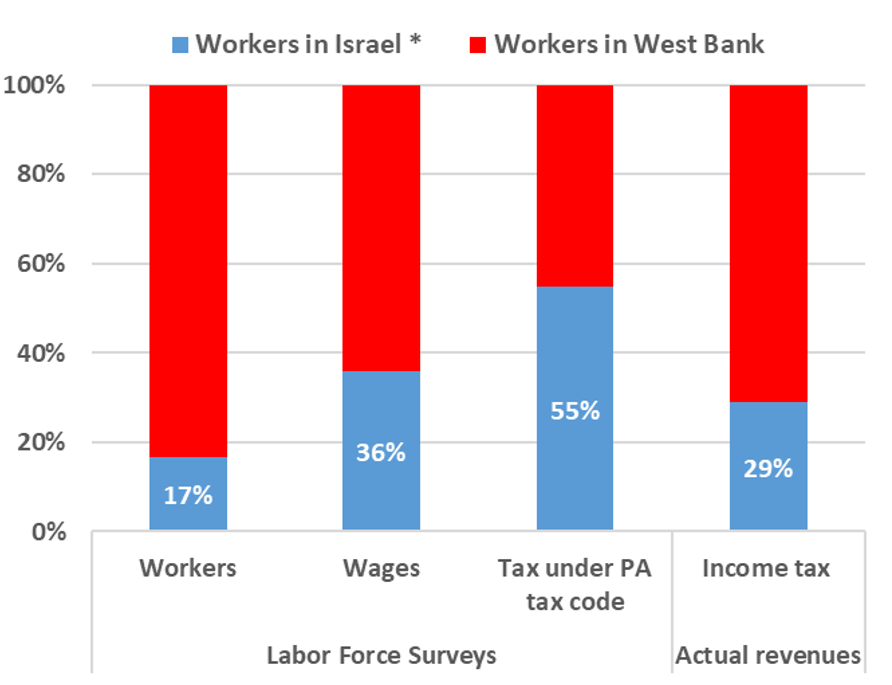

Figure 2 depicts the share of workers in Israel in total West Bank employment, wages, and income tax revenues in 2021. The graph’s first bar shows that 17 percent of West Bank workers were employed in Israel or in the settlements. The second bar shows that the total earnings of these workers account for 36 percent of the total employment earnings of West Bank workers. If workers employed in Israel or in the settlements would pay taxes according to the PA tax code, the tax revenue from these workers would account for 55 percent of the PA’s overall income tax revenue (see bar 3). This is because, Palestinians employed in Israel earn twice as much as those employed in the West Bank. Yet the last bar shows that when workers in Israel pay taxes according to the Israeli/Jordanian tax code, their revenue accounts for only 29 percent of the total income tax revenue.

* Includes workers in Israeli settlements in the West Bank

Figure 2: Share of workers in Israel and Israeli settlements in total West Bank employment, wages, and income tax revenues | Source: INSS analysis of Palestinian Labor Force Surveys and Palestinian Ministry of Finance.

Benefits of Taxing Worker Entry Permits

Our proposal is to tax Palestinian workers in Israel by attaching a fix price to entry permits instead of taxing them according to the Israeli/Jordanian tax code. This policy would shift the regulation of the number of Palestinian workers away from an exogenously determined quota into a system that takes into account the supply and demand of Palestinian workers in Israel. A change in the system will lead to several improvements over the current situation:

- This policy will generate greatly needed revenues for the PA. For example, a monthly fee of NIS 700 per permit on 150,000 Palestinian workers generates revenues of NIS 1,250 million instead of the NIS 250 million that the current system generates. This increase in revenues covers a third of the PA’s current deficit. The fee will also narrow the net-wage gap between workers in Israel and those in the Palestinian economy. This is a fair and progressive policy that brings about a decrease in income inequality. Workers earning higher wages will pay higher taxes relative to workers earning lower wages.

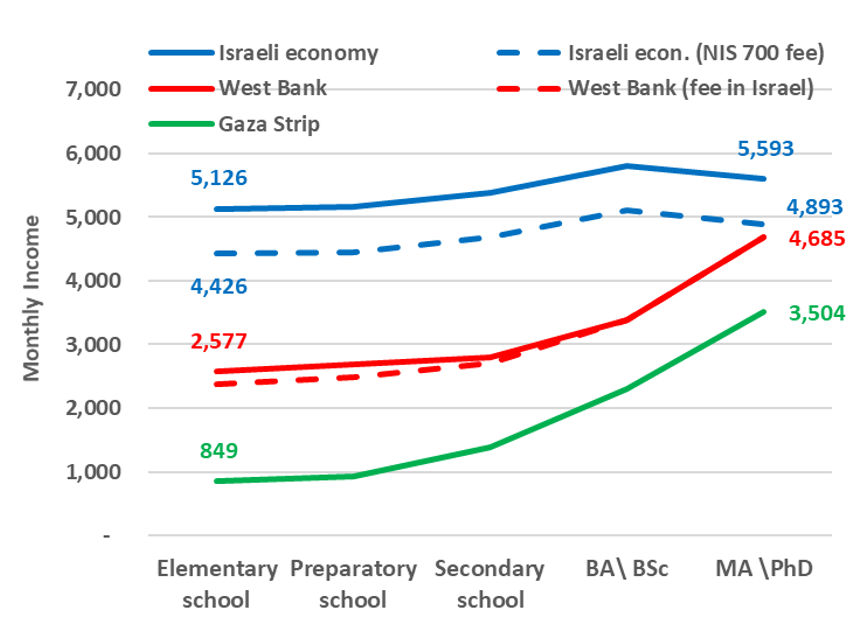

- Imposing a tax on entry permits will boost the Palestinian economy and local businesses. Palestinian workers in Israel are employed in low-skilled tasks. Yet as figure 3 shows, the wage gap between Israel and the Palestinian economies not only attracts low-skilled workers; it also leads skilled Palestinian workers to low-skilled jobs in Israel. This lowers the number of skilled workers and the productivity of the Palestinian economy. In addition, it shrinks the supply of workers in the Palestinian economy and leads to an increase of local wages (especially among low-skilled workers), which harms Palestinian businesses and entrepreneurs. Relatively well-paid low-skilled jobs in Israel also reduce incentives for schooling, which may cause a permanent reduction of skilled Palestinian workers in the long run. Figure 3 shows that a NIS 700 tax would not discourage high-skilled workers from taking low-skilled jobs in Israel. The size of the tax should be adjusted accordingly if the Palestinian Authority would like to discourage Palestinians with high human capital from taking menial jobs in Israel.

Figure 3: Monthly wage of male workers by place of employment & education, 2021 | Source: INSS analysis of Palestinian Labor Force Surveys

- It incentivizes the PA to cooperate with Israel on the regulation of entry permits and against undocumented work because the PA receives the tax revenues in their entirety.

- It reduces Palestinian workers’ incentives to buy entry permits illegally. Last year, 44 percent of permit holders made a monthly payment of NIS 2,450 to brokers for their permit. Around NIS 1,500 were used to pay for the worker’s social security, pension, and health insurance, while the broker (and his associates) pocketed the remaining NIS 1,000. Overall, we estimate that brokers’ total yearly revenue from this illegal trade was around NIS 1.2 billion. The policy we recommend basically shifts this revenue from illegal brokers to the PA’s coffers.

- It reduces the potential tax base for Hamas from Gazans working in Israel. Israeli authorities suspect that Gazans employed in Israel have to pay taxes to Hamas to allow them to cross the border. Those taxes are probably a function of the wage gap between employment in Israel and employment (or lack thereof) in the Gaza Strip. Imposing a price on permits reduces this gap.

- It is a simple policy to implement) recommended imposing a 38 percent tax on wages earned in Israel. Unlike the UN’s recommendation, the tax that we recommend does not require the cooperation of Israeli employers and can be collected directly by the PA.